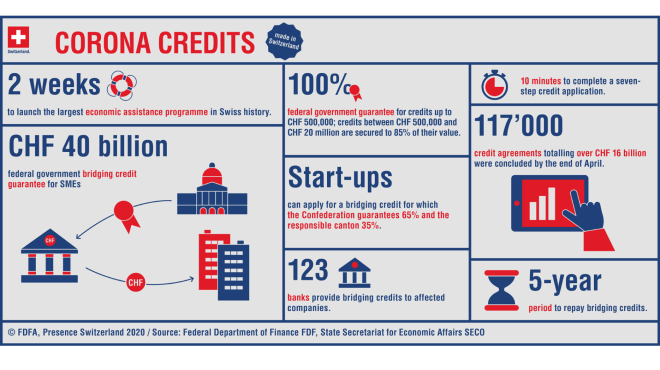

Simple, fast and efficient: Swiss COVID-19 bridging credits for companies in need

In record time, the Swiss government and the Swiss banks have rolled out an emergency programme to provide bridge loans to companies against the risk of illiquidity due to the Covid-19 measures. The figures now show: Over eight out of ten Swiss francs loaned were granted to microenterprises and small companies – mainly by the two largest Swiss banks and the cantonal banks.

On 25 March 2020, the Federal Council presented an emergency relief scheme involving guaranteed COVID bridging loans to support SMEs encountering liquidity problems due to the coronavirus. The scheme was established in close cooperation with the Swiss banks. The government-accredited loan guarantee organisations enable easy access to bank loans for SMEs (Find all information on the guaranteed COVID-19 bridging loans programme on line).

The loans were quickly brought to the companies in need because the following principles were applied: (1) take a pragmatic approach, (2) use established networks, (3) implement the action in a decentralised way and (4) insure compliance at a later stage to avoid backlogs in the deployment of the programme.

How the scheme works

Affected companies can apply to their banks for bridging credit facilities representing a maximum of 10% of their annual turnover and no more than CHF 20 million. In essence, the applicants fill out a one-page form with readily available information and identification. The applicants must meet certain minimum criteria. In particular, the company must declare that it is suffering substantial reductions in turnover because of the COVID-19 pandemic.

There are two credit facilities available:

- COVID-19 credits up to CHF 500,000 are fully secured by the Confederation and are paid out quickly and with a minimum of bureaucracy. It takes 10 minutes to fill out the credit application form, available online (https://www.easygov.swiss/easygov/#/en/landing/covid). The company then signs the printed credit agreement and sends it online or by mail to its house bank which pays the money within a day after reception of the agreement. For credits up to C500’000, Zero interest will be charged.

- COVID-19 plus credits exceed CHF 500,000. They are secured by the Confederation to 85% of their value; the lending bank secures the remaining 15%. Each company can obtain a credit of this type for up to CHF 20 million. A company must first submit a COVID-19 credit before it can apply for a COVID-19 plus credit exceeding 500,000 Swiss francs. However, a more rigorous bank review is required, and the guaranteeing organisation must issue a guarantee before the amount can be paid out by the lending bank. The interest rate on these credits is 0.5% on the loan secured by the Confederation. Companies with a turnover of more than CHF 500 million are not covered by this programme.

Large banks provide credits for small businesses

The Federal Department of Finance developed the emergency relief scheme in close cooperation with the banking sector thereby using established networks for crisis situations. 123 Swiss banks are lending COVID-19 credits to SMEs in need. As many SMEs only have a bank account with PostFinance, the financial services unit of Swiss Post was permitted to give COVID-19 credits to their clients as a temporary measure, thus applying the principle of pragmatism.

By 24 June 2020, 128’517 companies have received COVID-19 credits with a total amount of 13,300 Mio. Swiss francs. 729 COVID-19 plus credit applications with a total amount of 2,030.5 Mio. Swiss francs have been submitted so far. In a recently published analysis, SwissBanking revealed that 47% of the credit volume went to micro companies (0 – 9 employees) and 35.7% to small companies (10 – 49 employees). On the other side, the bulk of the credits was given by the two big Banks UBS and Credit Suisse (38.9%) as well as the cantonal banks (31,5%). It is a fine example how particularly large and financially solvent banks can help small businesses to survive difficult times.

Fraud is the exception

Although the procedure for companies to obtain a COVID-19 credit is exceptionally easy and fast, not many cases of fraud have been documented so far. After having investigated over 94,000 COVID-19 credits with a total volume of 11.4 billion Swiss francs, the Federal Audit Office (SFAO) has found indications for possible fraud in 400 cases covering a credit volume of 88 million Swiss francs. This is less than 1 per cent of the total credit volume. For most cases it is about dividends paid, double payments and false statements on turnover. One of the reasons is certainly, that in applying the principle of decentralised procedures, the credits are given by the house bank of the company which knows its clients well and can estimate the fraud risk more accurately than a centralised federal administration. Companies are also aware, that the administration and the banks have the necessary resources to persecute possible fraudsters at a later stage. This helps keeping fraud to a minimum.

An emergency programme, not on long term assistant scheme

COVID-19 credits are given with a payback period of five years. The intention of the federal government and the banks was to provide companies in Switzerland with liquidity immediately and over a short period to help with the economic consequences of the coronavirus. The programme therefore ends on 31st July 2020. However, such a programme is not adequate for long term purposes. If the economic crisis is deeper and long term, automatic macroeconomic stabilizers (e.g. short-time work, unemployment benefits) and good political framework conditions help the economy to recover.